Table of Contents:

Understanding 529 Plans and Their Flexibility

Rolling Over Unused Funds into a Roth IRA

Changing the Beneficiary

Using Funds for K-12 Education

Paying Off Student Loans

Withdrawing Funds for Non-Educational Purposes

State-Specific Programs and Incentives

Consulting with a Financial Advisor

Saving for a child's future education is a financial goal for millions of families, but circumstances sometimes change. Whether your student receives a scholarship, chooses an alternative career path, or simply doesn’t need the full amount saved, you may find yourself wondering what to do with unused education savings. Understanding your options, from repurposing funds to minimizing taxes, can help maximize the value of these thoughtfully accumulated resources. For Canadian readers, a common question is: What happens to an RESP if not used? Similar principles apply to U.S. 529 plans and other education savings accounts globally.

Unused education funds don’t have to be wasted. By knowing your plan’s features, legislative updates, and alternative uses, you can transform leftover savings into valuable assets for your family’s financial future. Whether it's helping another family member, funding K-12 tuition, or even rolling over into a retirement savings account, your next steps can make a significant difference.

Early exploration of these choices ensures that your hard-earned education savings will support future goals, even as circumstances shift. The strategies discussed here offer practical solutions that take recent legislative changes and specific plan rules into account.

Understanding state-specific programs, federal laws, and potential penalties will help you avoid costly mistakes. Always consult a financial professional to tailor strategies to your circumstances, but start here for an overview of the main options available to families today.

Understanding 529 Plans and Their Flexibility

529 plans are one of the most widely used tools for education savings in the United States. These tax-advantaged accounts allow you to invest for future qualified education expenses, including college tuition, trade school programs, and even some K–12 tuition expenses. Notably, the earnings within a 529 plan grow tax-free, and withdrawals used for qualified expenses are also tax-free, making them a powerful way to save.

Rolling Over Unused Funds into a Roth IRA

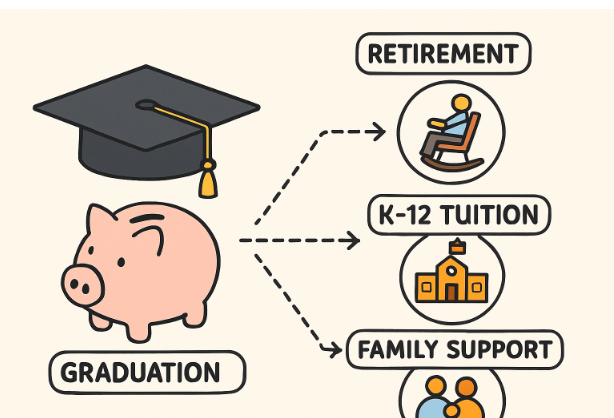

One of the most significant recent updates is the SECURE 2.0 Act, which allows families to roll over up to $35,000 of unused 529 plan funds into a Roth IRA for the same beneficiary (if the account has been open for at least 15 years). This innovative policy provides a valuable bridge from education savings to retirement security for young adults who might not require all their education funds for school.

Changing the Beneficiary

If your original beneficiary no longer needs the funds, 529 plans allow you to designate a new beneficiary from among eligible family members. This flexibility ensures that the savings can still benefit siblings, cousins, or even yourself if you wish to return to school. Changing the beneficiary typically does not incur taxes or penalties as long as the new beneficiary is within the eligible family category, as defined by plan guidelines.

Using Funds for K-12 Education

Recent legislation now allows families to use up to $20,000 per year from a 529 plan for K-12 tuition expenses at public, private, or religious schools. This expansion gives parents more immediate uses for their savings and makes 529 plans more versatile. However, state rules vary, and it’s wise to check your local laws for specific limitations.

Paying Off Student Loans

Under the SECURE Act, you can use up to $10,000 from a 529 plan to repay the beneficiary's student loans. This can significantly reduce education-related debt without losing the tax advantages on those distributions. However, this is a lifetime limit per beneficiary, and not all states conform to federal rules—so verify with your plan provider before making these withdrawals.

Withdrawing Funds for Non-Educational Purposes

If you need to withdraw unused funds for non-educational reasons, be aware that the earnings portion of the withdrawal will typically be subject to federal income tax and a 10% penalty. Some exceptions—such as the beneficiary’s death, disability, or receipt of a scholarship—may waive the penalty but not the tax. Weigh this option carefully, as it is usually the least efficient way to spend leftover funds.

State-Specific Programs and Incentives

Many states offer additional flexibility for unused education funds. For instance, Illinois allows residents to roll unused 529 funds into certain retirement accounts without penalty, while some states offer refunds or credits if your child receives a scholarship. Always check your state’s specific regulations and incentives to take full advantage of available benefits.

Consulting with a Financial Advisor

The rules governing 529 plans and other education savings accounts change frequently, and tax implications can be significant. Consulting with a qualified financial advisor is the best way to personalize your strategy and avoid costly mistakes. They can evaluate your family’s unique situation and help you make confident, well-informed decisions.

Unused education savings don’t have to be a sunk cost. With thoughtful planning and an understanding of the latest laws and plan features, you can turn surplus education funds into meaningful financial opportunities for your family’s future.

Want to add a comment?