PLPD insurance covers damage and injuries caused to others when you are at fault in an accident. This insurance does not protect your own vehicle or cover your own medical expenses. State-mandated coverage requirements can influence the amount and type of protection you need. What Is PLPD Insurance? Coverage Details Limitations of PLPD Insurance State-Specific Requirements Comparing PLPD and Full Coverage Is PLPD Right for You? ConclusionKey Takeaways

Table of Contents

Personal Liability and Property Damage (PLPD) insurance holds a distinct place in auto insurance, especially for drivers seeking practical and cost-effective options. If you are uncertain about what PLPD insurance covers, understanding its benefits and limits can help you make an informed decision about your policy selection. For drivers wanting essential protection at the minimal required cost, PLPD offers basic legal compliance and shields you from bearing the financial fallout of accidents in which you are at fault. To learn more specifics about what PLPD insurance covers, it’s essential to be clear about its protections and exclusions.

Many drivers are required to purchase PLPD insurance in order to drive legally, but not everyone realizes that it does not offer protection for their own vehicle or for many other incidents. By breaking down what is included, when it applies, and how state laws vary, you can assess whether PLPD meets your needs or if expanding to broader coverage is necessary. Having the right level of insurance not only offers compliance but also peace of mind when out on the road.

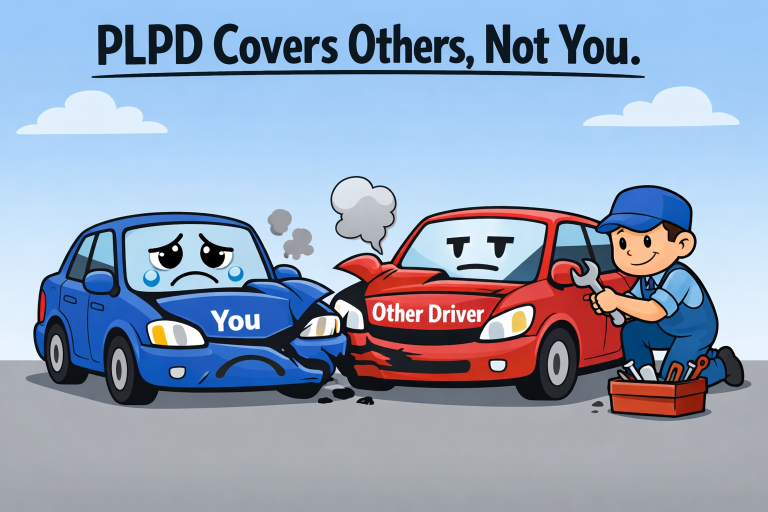

PLPD, or Personal Liability and Property Damage insurance, is the minimal form of auto insurance that allows drivers to legally operate a vehicle in most U.S. states. Its purpose is to cover the policyholder’s legal liability if they are responsible for bodily injuries or property damages suffered by others in an accident. In situations where you are found at fault, your PLPD insurance will help cover medical expenses and costs to repair or replace another person’s property, ensuring you aren’t left managing the financial responsibility alone.

Unlike more extensive insurance policies, PLPD is purposefully limited. It focuses solely on damage or harm inflicted on others, not on the policyholder’s own property or health. This structure keeps premiums affordable and supports compliance with state minimum insurance laws.

Understanding the specific coverage areas of PLPD insurance can help drivers identify where their protection begins and ends. PLPD consists of two crucial components:

Bodily Injury Liability: This section pays for medical expenses, lost wages, and potential legal fees for people injured due to an accident you cause. For example, if you injure a cyclist or another motorist, PLPD covers their medical bills up to your insurance limits.

Property Damage Liability: This covers the cost to repair or replace another person’s property if you are at fault. Damaged vehicles, fences, mailboxes, or buildings fall under this part of the policy.

When you cause an accident, such as rear-ending another car, PLPD will pay for the damaged vehicle and medical expenses for the individuals in the other vehicle, but only up to the amount specified in your policy limits. If the expenses exceed your limits, you could be held personally responsible for the balance.

The affordability of PLPD insurance comes with significant limitations. Knowing what is not covered is as important as understanding what is. Here are some common gaps in PLPD protection:

Damage to your own vehicle, regardless of fault, is not covered.

Your personal medical bills related to an accident are excluded.

Losses arising from theft, vandalism, fire, or other natural disasters affecting your car are not included.

To fill these protection gaps, drivers typically need to add additional options, like collision and comprehensive coverage, or consider a full coverage policy.

Each state sets its own minimum requirements for auto insurance, including the amounts and types of liability insurance drivers must carry. For example, in Michigan, the law requires drivers to have a minimum of $50,000 in bodily injury per person, $100,000 per accident, and $10,000 for property damage liability per accident. Not following these legal mandates can result in fines, license suspension, or even criminal charges.

Some states also operate under "no-fault" systems, in which personal injury protection (PIP) is required regardless of fault. Understanding your state’s laws is essential for not only staying compliant but also protecting yourself adequately. Reliable resources like Forbes' roundup of state minimum insurance requirements help keep you current and informed about changes in your state’s insurance landscape.

When deciding between PLPD and full coverage insurance, the decision centers on the scope of protection and personal risk tolerance. While PLPD only covers liability to others, full coverage adds the important elements of:

Collision Coverage: Pays to repair or replace your car in case of an accident, regardless of fault.

Comprehensive Coverage: Includes protection from non-collision events such as theft, vandalism, and weather-related damage.

Full coverage is particularly valuable for newer or higher-value vehicles and for drivers who want to minimize out-of-pocket risk after an accident or non-accident event. It delivers greater peace of mind but also comes with higher insurance premiums.

The decision to stay with PLPD or upgrade to more comprehensive insurance will depend on several personal factors, including:

Vehicle Value: Older vehicles may not merit the cost of full coverage, since repairs could exceed the car’s value.

Financial Situation: If you can afford to repair or replace your car after an accident, PLPD could be sufficient. If not, more coverage might be necessary.

Driving Habits: High-mileage drivers or those in areas with more accidents may want additional coverage for greater risk mitigation.

Assessing these considerations can help you find a balance between affordability and the level of protection needed to keep your finances and peace of mind intact.

PLPD insurance stands as a fundamental offering for drivers seeking basic protection and legal compliance. It primarily protects you from the financial fallout of damages and injuries you cause to others, but does not offer benefits for your own losses. By understanding both the strengths and gaps of PLPD, along with state-specific insurance requirements, drivers can make smarter choices when selecting or upgrading their auto insurance to stay protected on the road.

Want to add a comment?